- What is a Chargeback?

- What is Chargeback Fraud?

- What is the True Cost of Chargeback Fraud?

- How to Protect Your Organisation from Up to 100% Chargebacks

- Achieve Further Savings by Securing Your Transactions and Unlocking a Better Rate

- Frequently Asked Questions

- Reduce Chargebacks in Your Organisation

How to Reduce Fraudulent Chargebacks

What are chargebacks and how can you protect your organisation?

Table of Contents

What is a Chargeback?

Chargebacks are a form of consumer protection, when a transaction is reversed as a result of a disputed debit or credit card purchase.

A consumer can claim back money for their purchase if the goods are damaged, not as described, haven’t been delivered or if they have proof they didn’t make the purchase in the first place. If the dispute is successful, the issuing bank withdraws the funds they previously deposited into the recipient account.

This scheme encourages the provision of quality goods and services to consumers, but can leave businesses exposed to various methods of fraud, which may have significant financial impact.

What is Chargeback Fraud?

Chargeback fraud, also referred to as “friendly fraud”, occurs when a consumer makes a legitimate purchase with a credit card, then requests a chargeback from their bank. If it’s approved, the consumer not only keeps the purchase, but has also received a full refund.

Well intentioned customers may accidentally commit friendly fraud because they don’t know how to reach out to the company for a refund or discuss an issue with the order. However, other “cyber shoplifters” look to exploit the chargeback process in an attempt to get “free” products and services from a business.

Alternatively, contact us now to see how we can help:

+44 (0) 1302 513 000 or sales@keyivr.com

What is the True Cost of Chargeback Fraud?

Not only is the cost of goods lost from fraudulent chargebacks, there are additional financial implications for organsations, such as:

- Chargeback fees issued by the bank against the organisation

- Non-refundable transaction fees from the Gateway or Acquirer

- Non-refundable shipping costs for physical goods

- Unrecoverable salary and bottom-line costs for services

- Valuable time and resources used to process and dispute charges

The Impact on U.K. Businesses:

Visa recently reported 70% of chargebacks were actually fraudulent.

If a UK business receives too many chargebacks they could face increased transaction fees and rates from their Gateway or Acquirer. They also risk being prevented from taking payments by certain methods all together (such as over the phone or other MOTO channels).

How to Protect Your Organisation from Up to 100% Chargebacks

We have developed a secure payment service called Click 3D that uses a range of features to risk assess a purchase and help authenticate the identity of a customer. The level of ‘risk’ applied to each Card-Not-Present (CNP) MOTO or Ecommerce transaction can be unique to your organisation, how you take payments (online, over the phone, webchat etc) or for each individual customer.

Here’s how you can protect your organisations from up to 100% of all chargebacks, no matter what payment channel your customer is using:

How to Protect Ecommerce (ECOM) Transactions from Chargebacks

The crucial step in reducing fraud online is verifying the identity of the customer. This is not only to protect against stolen credit card information being used, but also will also protect your organisation from legitimate online purchases becoming a fraudulent chargeback.

Additionally, you need to protect your organisation from returning customers who have made fraudulent chargebacks in the past, so they can’t do the same for future purchases.

By adding 3D Secure (also known as 3DS) to ‘high risk’ transactions, an identity verification service supported by all major debit and credit card issuers, you can dramatically reduce the amount of fraudulent transactions and chargebacks. The risk criteria can also be configured to wipe out chargebacks completely, ensuring all online payments are verified with 3D Secure.

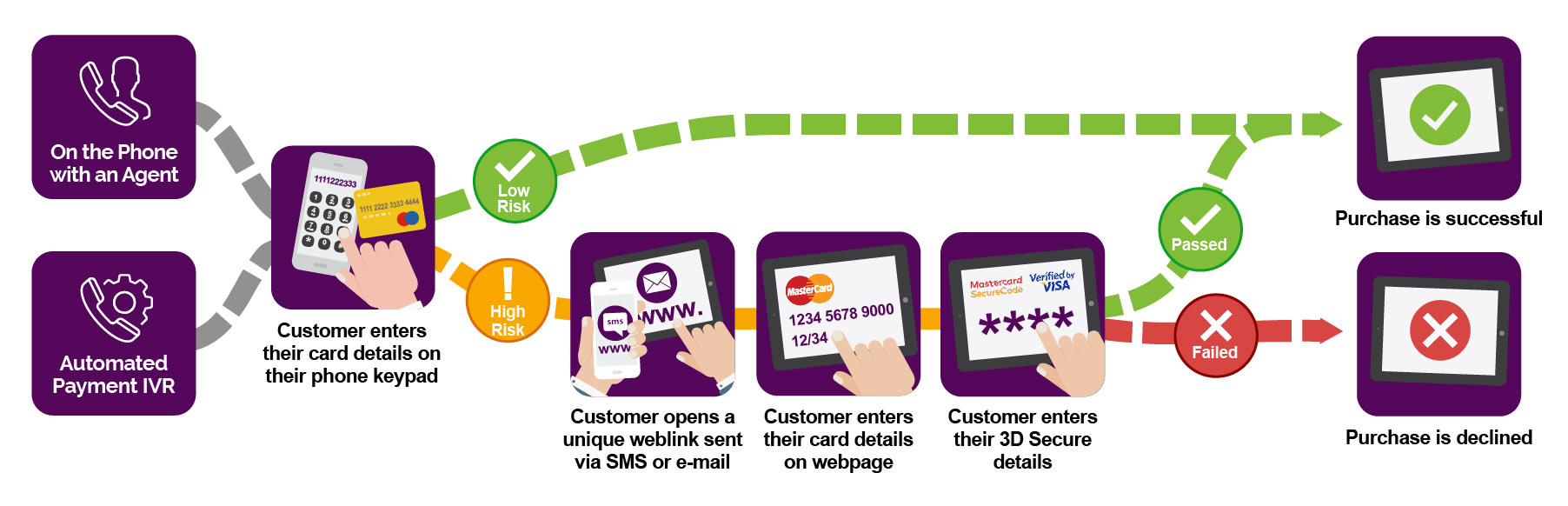

How to Protect Mail Order / Telephone Order (MOTO) Transactions from Chargebacks

For MOTO payments made over the phone or through an automated IVR, triggers can be put in place that assesses the risk of the transaction. If it’s deemed as ‘high risk’, an SMS or email can automatically be sent to the customer with a secure weblink, requesting that they verify their identity through 3D Secure. The web page can be prefilled with all their card payment information they’ve provided, so once they’ve passed 3D Secure the purchase is easily completed online.

The aim of this approach is to convert ‘high risk’ MOTO payments into an identity verified Ecommerce (ECOM) transaction, considered to be more secure by Gateways and Acquirers. All transactions verified with 3D Secure can not be claimed as a chargeback.

Your organisation can determine what it considers to be ‘high risk’ to route customers appropriately, there are a number of ‘flags’ that can be set. It could be in place for all customers, for those purchasing a certain volume or simply for those who have made fraudulent chargebacks in the past.

Achieve Further Savings by Securing Your Transactions and Unlocking a Better Rate

Payment Gateways and Acquirers set their fees and transaction rates based on a number of factors, including security and risk. Key IVR have excellent relationships with a wide range of suppliers and can discuss the savings that could be unlocked by improving the security of your payments.

Frequently Asked Questions

The easiest form of transaction to make a chargeback against is a Card-Not-Present or Cardholder-Not-Present (CNP) transaction. These occur when the consumer isn’t present in person when making a purchase.

CNP transactions can occur online, where card details are typed in and the customer’s identity isn’t verified – these are classified as CNP Ecommerce payments.

Alternatively, card details can be given over the phone to a contact centre agent or keyed into an automated IVR – these are known as CNP Mail Order / Telephone Order (MOTO) transactions.

The merchant may not have verified the identity of the person using the credit card, either because it’s quite difficult and costly to do, or it adds a large obstacle to the shopping experience for all customers. Unfortunately, many organisations struggle to combat chargebacks against these type of transactions as they have limited evidence to prove the purchase was made legitimately.

Card-present transactions involve Chip and PIN payments, contactless/NFC or Mobile wallet payments, essentially payments where the customer is physically with the merchant when making the payment and able to verify their identity.

The key to reducing fraud is to take CNP transactions and high risk payments through a verification process to authenticate the customer. With Click 3D not matter how a customer wants to pay (online, over the phone, over email, etc) steps can be put in place to help protect the organisation.

3D Secure, or 3DS, is a service that helps card issuer banks authenticate the identity of online purchases. In order to complete the payment, a customer is prompted to enter a password that was created when the card was first registered.

For Visa, the service is called Verified by Visa, Mastercard has a similar system called Mastercard SecureCode and American Express has a solution called SafeKey.

An organisation can decide if it wants to use 3D Secure within it’s payment process, what the risk factors are that will trigger the service and how secure they want to make the transaction.

Using 3D Secure is a crucial step in reducing fraudulent chargebacks and credit card fraud overall.

The definition of “high risk” transactions can vary from business to business. It can depend on the type of products and services they offer, what industry or countries they operate in, the nature of their customers and finally how they take payments. What an organisation considers “high risk” may be different to their bank or PSP which sets the fee and percent rate for every credit or debit card transaction they process. For example, payments made over the phone where the customers’ identity can’t be verified are considered a higher risk to those which have passed through extra security steps, such as 3D secure.

High Risk:

- CNP MOTO and ECOM payments where an identity isn’t verified.

- No Address Verification Service (or AVS) match in place.

- Customer has a high number of failed payments – which could indicate stolen credit card information.

- Customer has made fraudulent chargebacks in the past.

- Customer places a large order with high value.

Low Risk:

- ECOM payments with a verified identity – 3D Secure can assist with this.

- Address Verification Service (or AVS) match is in place with the payment gateway.

- Customer has no or a small number of failed payments.

- Customer hasn’t fraudulent chargebacks in the past.

- Customer places frequent and regular orders, they may even have their card saved against their account.

Chargeback fraud occurs when a customer uses their card to make a legitimate purchase, to only then claim it as a chargeback, sometimes stating it wasn’t them who made the purchase. The goal being to keep the goods or to have still used a service without paying.

Credit card fraud occurs when someone uses stolen card details to purchase goods and services, leaving the victim to pay the bill. If a business doesn’t take the necessary steps to verify the customer’s identity, then they are obligated to refund the fraudulent order if a chargeback is claimed.

If you’re looking to protect your customer’s sensitive card details from potential credit card fraud, PCI-DSS accredited payment services can process valuable card holder data without it entering your organisation’s environment.

Reduce Chargebacks in Your Organisation

Talk to us about the many options available in reducing the number of chargebacks impacting your organisation. We’ll discuss how you currently take payments and the steps you could consider across your MOTO and ECOM payment channels to save valuable time and recover lost business revenue.

We also have an excellent relationship with major payment Gateways and Acquirers, so we can work with you and unlock better transaction rates, resulting in significant savings.

Submit your details below and a payment expert will be in touch:

Alternatively, call +44 (0) 1302 513 000 or email sales@keyivr.com.

Key IVR are a privately owned business offering global automated PCI-DSS compliant payment services. We are a customer-service focused organisation and take care to manage and meet our clients' expectations.